We have been hearing about blockchain for several years now, yet its adoption is still not very common. The purpose of this article is to investigate its causes, proposing the use of low-code as an effective remedy.

Brief history

The mechanism behind the blockchain was first conceived in 1991 by researchers, as well as cryptographers, Stuart Haber and W. Scott Stornetta, with the precise intent to mark digital documents with a timestamp, certifying the date of creation. The aim was to guarantee the immutability of the document, avoiding possible alterations or backdating. In this way it was possible to resolve once and for all issues related to intellectual property rights, a fundamental goal for a world increasingly oriented towards digitization. The solution proposed by the two researchers was divided into two phases. Initially the document was assigned a unique ID, produced by a cryptographic hashing algorithm.

This would certify the immutability, because if you changed even one bit of the file, its ID would be completely different. Then the hash value was sent to a time-stamping company, to use the TSS (Time Stamping Service). The company would mark it with date and time, sign it by digital signature and finally send it back to the customer. By checking the signature the customer was sure that the hash had been received correctly and that the correct time and date were included [1]. One year later, in 1992, the system was improved thanks to the introduction of hash trees, also called Merkle trees (by Ralph Merkle who obtained the patent in 1979), able to efficiently and securely verify large data structures (no longer individual documents) by comparing the hashes of the same. At the end of October 2008 on “Cryptography”, a mailing list of cryptography enthusiasts, on metzdowd.com, was published “Bitcoin: A Peer-to-Peer Electronic Cash System”, a white paper introducing a decentralized peer-to-peer electronic money system called Bitcoin. The author of the document, whose identity is not yet known and whose pseudonym is Satoshi Nakamoto, cited eight articles related to his work and three of them were signed by Haber and Stornetta. It was 31/10/2008 and it was precisely this date that marked the official birth of the blockchain. A year later, in 2009, the first version of Bitcoin software was distributed and in 2010 the first transaction took place… a pizza!

A lot of interest and a lot of experimentation. But the implementation projects?

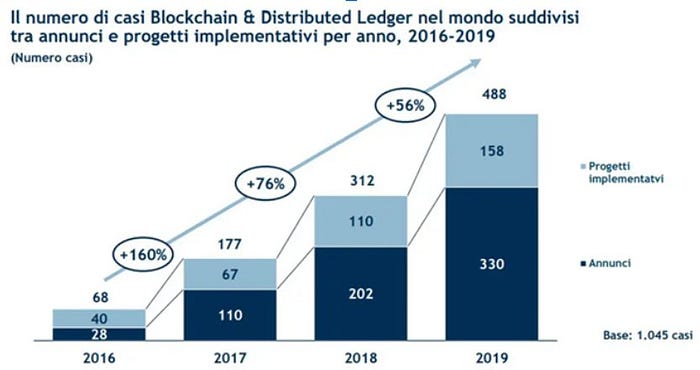

In recent years the interest around the blockchain has grown considerably. From what emerged from the Observatory Blockchain & Distributed Ledger of the Politecnico di Milano, 2019 was the year of confirmation of the importance of this technology. There are 488 Blockchain and Distributed Ledger projects launched around the world (which bring the number of projects in the last 4 years to 1,045), an increase of 56% compared to 2018.

Osservatori.net digital innovation [2]

The numbers show how this sector is marked by a high degree of interest and experimentation, also motivated by the enormous media attention that has emerged in recent years. At the same time as these data, certainly positive and promising, it is necessary, however, to take into account also those that arouse some doubt and concern, i.e. those related to implementation projects. In fact, of these 488 projects, only 158 are implementative (of which only 47 are already operational, the rest are proof of concept), while 330 are only announcements. The question that arises spontaneously is: “why are they so few despite the great interest?

Barriers to adoption

Like any new technology, the blockchain has had to and is still facing many challenges that undermine its spread. Let’s see them in detail.

Lack of a solid understanding of technology: this is without a doubt the biggest hurdle to overcome. The blockchain is a technology, defined by many, too complex to stimulate the interest of the masses. Appropriate training courses are needed to develop the specific skills needed to operate in such an area. Paths that require a certain investment of resources, especially in terms of time and money, which currently companies do not intend to employ. At the organizational level, in fact, many managers have shown a certain degree of reluctance to use technology. This is mainly due to the scarcity of successful use cases and forecasts of a lack of economic return on investment in this area. This lack of willingness to study and understand the blockchain has caused a shortage of qualified talent, as well as an inadequate perception of the real benefits and advantages of its adoption and that of the various viable use cases. In fact, currently, it is common practice to approach the blockchain exclusively to cryptocurrency or, more generally, to the world of finance. In fact however, the areas of application are numerous and even deeply heterogeneous.

Normative adaptation: also from this point of view there is a strong lack, in particular the felt need for a suitable regulatory system to regulate and regulate the use of technology in various areas. Just as there is a lack of support and collaboration from government authorities towards all those organizations that wish to implement it within their business. A clear and concrete regulatory framework together with constant support from the authorities would benefit the spread of the blockchain, as this combination would certainly have the power to encourage more experimentation. It is also important to consider that one of the greatest advantages of using the blockchain is to be able to do without trusted brokerage figures, most of which are an integral part of the current regulatory fabric. This may partly justify the delay made by government authorities in implementing regulatory compliance.

Adaptation of computer systems: we are talking about a fairly recent and not yet mature technology. Most organizations, before being able to use it properly, are forced to transform and adapt current information systems so as to allow proper interaction with technology, or to procure/develop independently blockchain solutions that can communicate with them.

Initial costs: one of the very first obstacles to overcome in reference, above all, to small and medium-sized companies. Knowledge, training, skills development, software updates, etc.. These are all feasible objectives, but only through major investments and especially if the forecasts of the relative economic return are realistic. In addition, the novelty and complexity characterizing the blockchain do nothing but expand these costs. The adoption of the technology requires the development of a proprietary solution or entrusting it to a blockchain service provider, currently few in number. This is without even mentioning the cost of hiring qualified professionals.

Privacy vs transparency: transparency is another of the main benefits of a blockchain network. In fact, transactions must be visible to all network participants. Although this is an advantage for many, others see it as a cause for repudiation. An example are governments, which, for various reasons, are forced to protect access to sensitive data. As a result, the mechanism of distributed consent and the requirement for transparency, although they are generally two of the driving forces behind the use of a blockchain network, are at the same time a barrier to certain parties.

Lack of recognized standards: to date there are few blockchain implementations recognized worldwide. Probably only Hyperledger and Ethereum represent the only infrastructure to have received acclaim as a standard in all industries. More standards would undoubtedly help accelerate the process of adoption of the technology.

Scalability of transactions: currently Bitcoin, the flagship application of blockchain technology, can perform a maximum of 7 transactions per second, although on average 3 to 4 transactions are processed. Wanting to make a quick comparison with a payment method recognized around the globe, you can find that VISA can handle 4000 transactions per second, while the ceiling is even 47,000. It is therefore clear that large-scale blockchain solutions will require technical improvements to the architecture behind the technology.

Trust issues: although features such as transparency, consensus mechanism and decentralization instill confidence in the technology, the link with illegal activities, often heard about in the media, hinders mass adoption. In reality there are few scientific studies that confirm these accusations (one of the best known is represented by the survey “Sex, Drugs and Bitcoin: How Much Illegal Activity Is Financed Through Cryptocurrencies?” conducted by Sean Foley of the University of Sydney, Jonathan R. Karlsen of the Polytechnic University of Sydney and Tālis J. Putniņš of the Stockholm School of Economics in Riga), while there are many more who claim otherwise (a survey by Cornell University, for example, explains that using cryptocurrencies for illicit purposes is even more risky than using traditional channels). [3]

Effects related to mass behavior: this is an obstacle closely related to the previous one. It refers in particular to the bandwagon effect, whereby individuals make certain choices or actions exclusively because they are taken by most other people. If for personal gain many media say that the blockchain is used for illicit purposes, or several prominent figures of major companies say that it is a very complex technology, such reputation will tend to stick to the technology. The bandwagon effect will only feed these beliefs.

Low-code, a short introduction

The term “low-code” was coined by Forrester in 2014 with the intent to label development platforms that focused on ease of application programming, known in the common language as “low-code development platform” or LCDP. As a result, it is possible to define low-code as a set of tools that allow the development of complete applications quickly and visually by performing simple “drag and drop” operations with the pointer of your mouse, eliminating the need to write hundreds of lines of complex code because it is the intelligence of the algorithm that takes care of converting the application into code. Among the main advantages you can include:

Speed of development: through a low-code platform it is possible to develop a functional software up to 10 times faster.

Low costs: the great speed benefits companies because it significantly reduces development costs, while freeing up valuable resources to be used elsewhere.

Ease of use and development: The graphical user interface provided by an LCDP not only makes it easier to develop applications thanks to the various tools offered, but also makes it easier to learn and use the platform itself. The resulting benefit is twofold, since on the one hand professional developers are able to accelerate programming speed, on the other hand even users with little or no professional software development expertise are able, after a short training period, to create an application suited to their needs.

Applying these advantages to the blockchain could be the key to overcome those obstacles that limit the enormous potential of this technology, not yet understood and fully exploited.

Low-code & Blockchain: a winning duo

It would be hypocritical to say that the low-code can act as a panacea, able to break down all the barriers mentioned above. Some can be overcome only with a greater collaboration between companies and authorities, others only through a greater degree of maturity of the technology. Others, however, with the help of a valid ally such as the low-code, will no longer represent a problem. In an era where only those who are able to carry out sudden digital transformations survive, being agile is one of the prerequisites for success. The low-code was born to satisfy this growing need thanks to the simplicity and speed of development offered. If, as previously stated, one of the major limitations of the blockchain is its complexity, thanks to this winning combination creating a reliable blockchain network will be an extremely fast and easy operation. With low-code are directly addressed some of the main barriers to the adoption of the blockchain:

Any company facing sudden and challenging changes will be able to rely on a technology that can produce satisfactory results in a short time, incurring reduced costs and minimizing risks.

Experienced developers are often expensive and good talent is not easy to find. With low-code, even non-professional developers have the concrete possibility to give light to high technology and quality applications, while professionals will be made easier in their job by being able to devote time to more projects, increasing productivity.

The graphical user interface and configuration modules offered by an LCDP allow you to shorten the learning curve of blockchain technology, replacing the traditional operation of writing source code. The proverbial complexity coupled with blockchain is now less scary.

Thanks to low-code you can share the blockchain network project with other members in the form of self-documented material, consisting not of strings of code but the representation of the network structure in graphical form.

The tools and validation mechanisms of these platforms are able to immediately report any errors during the design phase of a smart contract or blockchain network, without necessarily having to get to the testing phase, further accelerating their development.

We are convinced that blockchain type solutions will increasingly take hold within organizations, creating real ecosystems able to collaborate effectively through secure and reliable networks. We also think that the low-code will play a key role in this upcoming game, supporting and accelerating the spread of the blockchain phenomenon. And you? What do you think? Write it in the comments.

Curiosity pills!

The first Bitcoin transaction was made on May 22, 2010 by Laszlo Hanyecz who, on Bitcointalk Forum, wrote this announcement: “I’ll pay 10,000 bitcoins for a couple of pizzas… like maybe 2 large ones so I have some left over for the next day. I like having left over pizza to nibble on later. You can make the pizza yourself and bring it to my house or order it for me from a delivery place, but what I’m aiming for is getting food delivered in exchange for bitcoins where I don’t have to order or prepare it myself, kind of like ordering a ‘breakfast platter’ at a hotel or something, they just bring you something to eat and you’re happy!” Still today, every year we celebrate the so-called “Bitcoin Pizza Day”, just to celebrate the most expensive pizza ever, today worth just over 87 million euros!

Diana is the Head of Growth at AstraKode. With a background in business and marketing, she brings a practical approach to the team. Diana focuses on identifying growth opportunities and advancing Astr ... read more

Diana Levytska

Diana is the Head of Growth at AstraKode. With a background in business and marketing, she brings a practical approach to the team. Diana focuses on identifying growth opportunities and advancing AstraKode’s development within the tech industry.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" and our Privacy Policy" to provide a controlled and aware consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.